Make it to the major leagues, even for a cup of coffee, and you unlock one of the most generous retirement systems in all of professional sports. The MLB pension is famous for how fast it vests and how much it can eventually pay, and it is a big reason a single day in the big leagues is worth so much more than the salary alone. So how does the MLB pension actually work, how quickly do players qualify, and how much can they collect?

The short version is striking: one day in the majors earns lifetime health coverage, 43 days earns a lifetime pension, and ten years maxes it out at a six-figure annual benefit. The details, though, are where it gets interesting.

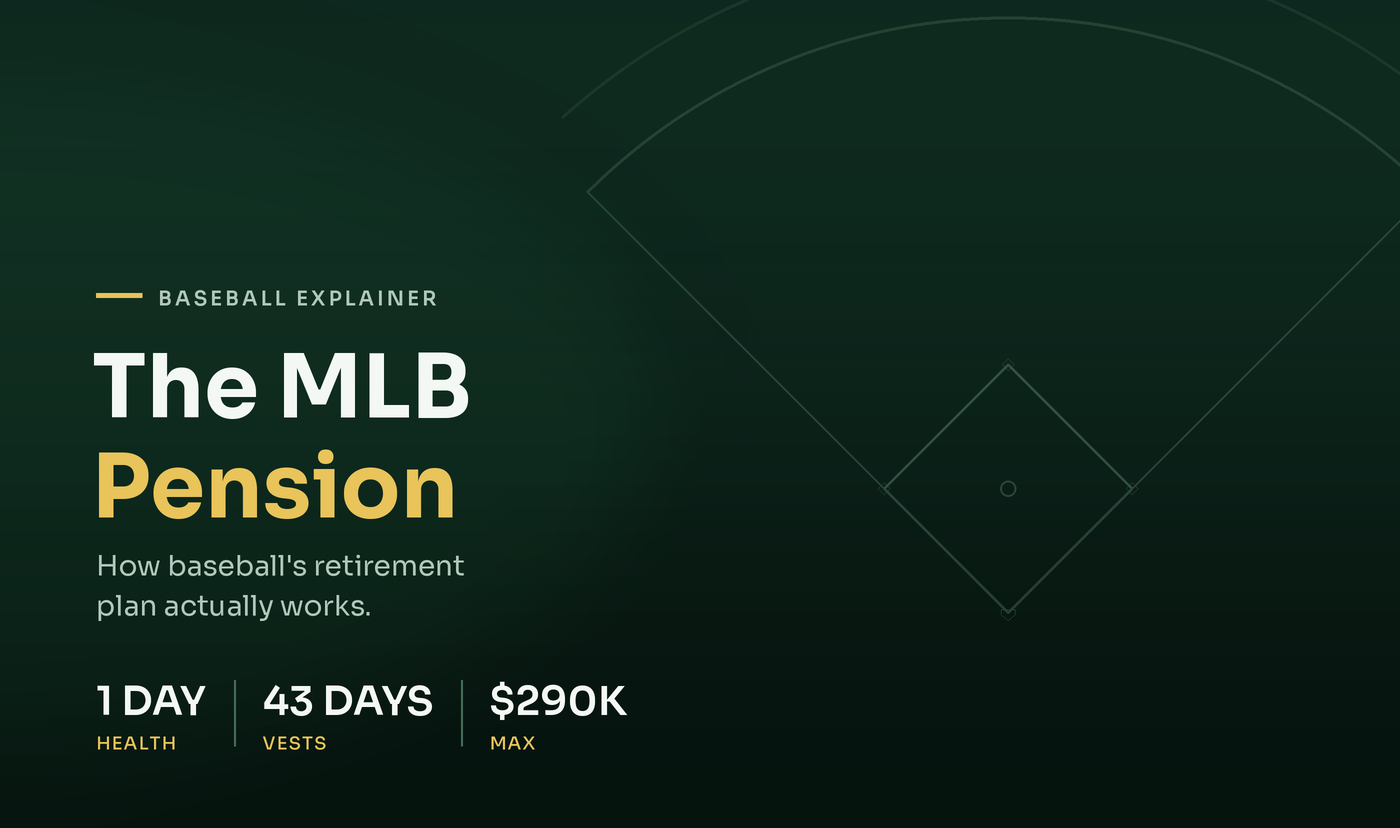

The chart below breaks down the MLB pension: the vesting milestones, the payouts, and how it compares to other leagues. Take a look, then we’ll explain each part.

How the MLB Pension Works

The MLB pension is a defined benefit plan, meaning it pays a guaranteed amount in retirement based on a set formula rather than on investment returns. The formula rewards major league service time, measured in days on an active roster or the injured list. What makes it so notable is how quickly it vests compared to other retirement plans. A player does not need a long career to lock in lifetime benefits; even a brief stint in the majors is enough to start. The plan is funded largely by owner contributions negotiated through the collective bargaining agreement between MLB and the players’ union, and it includes annual cost-of-living increases.

The Vesting Milestones

The most remarkable feature of the MLB pension is how fast it kicks in. Just one day on an active major league roster earns a player comprehensive health insurance for life. Pension eligibility begins at 43 days of service, which is one quarter of a season, and at that point a player has vested into roughly 2.5 percent of the maximum benefit. From there, every additional 43 days of service adds about another 2.5 percent. A player keeps building toward the maximum until they reach ten years of service, or 40 quarters, at which point the pension is fully vested at its highest level. A full season counts as four quarters.

How Much Players Can Collect

The numbers are eye-catching. In 2026, a player with ten years of major league service who waits until age 62 to start collecting can receive a maximum pension of about $290,000 per year for life. Players with less service time receive a prorated amount based on how many quarters they accrued. Players can choose to start collecting as early as age 45, but doing so reduces the annual payout, since the benefit will be paid out over more years. Waiting until 62 unlocks the full amount. On top of all this, the plan carries annual cost-of-living adjustments of roughly 1.8 percent, so the benefit keeps rising over time, a rarity among modern pensions.

How It Compares to Other Sports

What truly sets the MLB pension apart is its vesting speed. In the NFL, a player needs three credited seasons to qualify for a pension. The NBA also requires three seasons, and the NHL requires 160 games played. By contrast, an MLB player needs just 43 days. That difference is enormous: a baseball player who appears in the majors for part of a single season can secure a lifetime pension, while players in the other leagues must stick around for multiple full seasons. Combined with the one-day health insurance vesting, this makes even a short major league career far more valuable than the salary alone suggests.

The History Behind the Plan

The MLB pension was created by owners in 1946 and took effect in 1947, established partly to head off early efforts by players to unionize. For decades the benefits were modest and the vesting requirements steep, leaving many older players with little. The turning point came when the players’ association hired Marvin Miller as its executive director in 1966. Under Miller, a series of collective bargaining agreements transformed the pension, expanding benefits, adding health coverage, and slashing the vesting requirements. By 1980, vesting had been cut to one day for health insurance and 43 days for the pension, the thresholds that still define the plan today.

The Criticism: Minor Leaguers Left Out

For all its generosity, the MLB pension has a long-running blind spot: it only credits major league service. Minor league players, who are not part of the same union, do not earn the rich MLB pension no matter how many years they spend in the minors. A player can grind for a decade in the minor leagues and receive nothing close to what a teammate who logged 43 days in the majors gets for life. There are smaller, separate benefit programs for minor leaguers and for certain pre-1980 players who missed the modern vesting rules, but the gap remains significant and is a frequent point of criticism. If you enjoy these baseball explainers, see our breakdown of how MLB arbitration works.

The Bottom Line

The MLB pension is one of the most generous and fastest-vesting retirement plans in professional sports. One day in the majors earns lifetime health coverage, 43 days locks in a lifetime pension, and ten years of service maxes it out at roughly $290,000 per year in 2026. That fast vesting, far quicker than the NFL, NBA, or NHL, is what makes even a brief major league career so valuable. The plan is not perfect, most notably leaving minor leaguers out, but for those who reach the show, it remains one of the best benefits in all of sports.

Pension figures are set by the MLB collective bargaining agreement and adjusted over time. The amounts here reflect the most recent available data and are for general informational purposes, not financial advice.